Lookr

Lookr built AI engines that help businesses empower their customers to visualize and share their ideal products in seconds. By leveraging on-location spatial information and proprietary AI models, Lookr enabled photographers, journalists, and content creators to point their camera at any backdrop and instantly receive AI-generated location-specific inspirations — maximizing creative output in a matter of seconds.

I co-founded and served as CTO of Lookr, leading the development of the core AI engine and product architecture. As an AI researcher with publications in Nature, I focused on building the proprietary models that powered Lookr's real-time spatial understanding and visual inspiration generation.

Highlights:

- Selected as a top 0.5% finalist of the 500 Global Incubator in Palo Alto — one of the world's most competitive startup accelerators.

- Joined the University of Waterloo Velocity Incubator in fall 2023, gaining access to Waterloo's world-class founder network and engineering talent pipeline.

- Featured in University of Waterloo News and Velocity News.

- Invited to exhibit at LEAP 2024 in Riyadh, Saudi Arabia — one of the world's largest tech conferences with over 215,000 attendees and $13B+ in announced investments.

- Invited to the Canadian Embassy in Saudi Arabia by Ambassador Jean-Philippe Linteau during LEAP 2024.

Although we have since stepped away from Lookr, the experience of building a company from zero to international recognition — pitching at 500 Global, growing through Velocity, and showcasing at LEAP — was formative in shaping my approach to building technology at the frontier of AI.

DeepAlpha

DeepAlpha is a quantitative research firm applying scientific techniques, AI, and Quantum Computing to find patterns in large, noisy real-world financial data sets for making smart decisions. It provides data-driven portfolio management services for subscribed clients. The company was co-founded by an NYU professor and DeepMind ML Engineer.

Starting from May 2022, I was working in this firm as an Quantitative Researcher and Software Developer. I developed algorithms for portfolio management based on finanical-principle-aware Reinforcement learning, which became a core part of company’s own code base. I also collaborated with Software Development team, and we successfully built an end-to-end trading pipeline including financial data processing, Alpha factor engineering, ML model selection, strategy back testing, paper trading and online trading.

Here is a blurred screenshot of the trading pipeline we developed during my time-consuming but interesting work here, and it is a complete and robust pipelines (much less bugs than FinRL >.<):

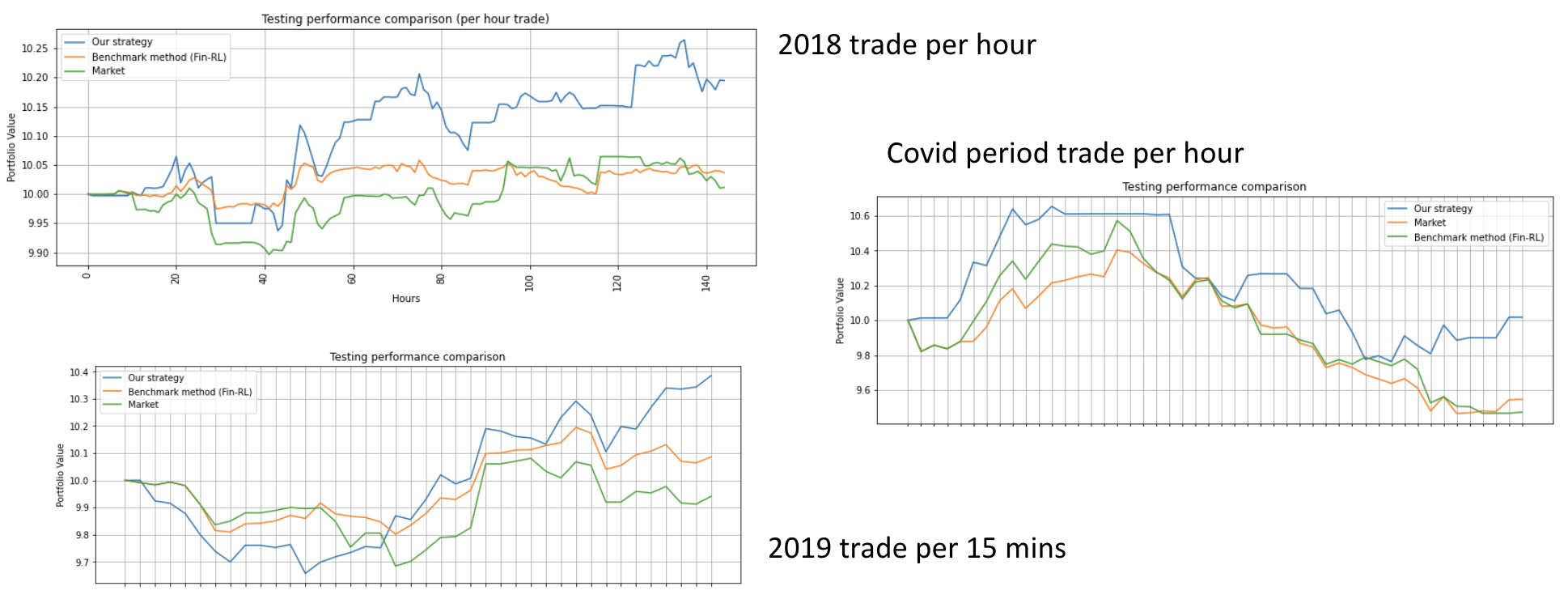

Also, we already did some intial testings on the customized RL algorithms that I developed over 6 months. Here is some particular results during backtesting:

We can see that the algorithms that I developed outperformed the market as well as famous FinRL packages built-in models in terms of portfolio value for testing period !! Besides, our modelled succeed to not losing or even making a little bit during Covid period.

We can see that the algorithms that I developed outperformed the market as well as famous FinRL packages built-in models in terms of portfolio value for testing period !! Besides, our modelled succeed to not losing or even making a little bit during Covid period.

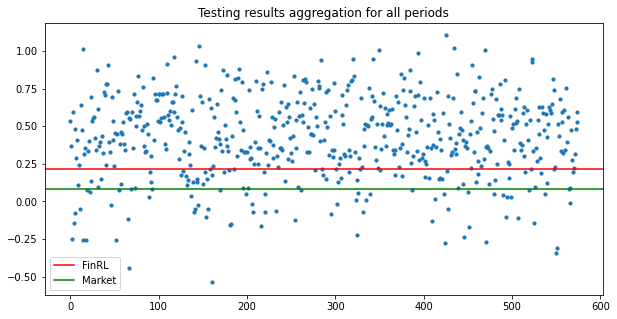

We extend this testing to more periods, and plot the testing period Sharp Ratio for all the periods, and compare them with average result for FinRL model Sharp ratio and the market Sharp ratio: